SMM May 29, 2025:

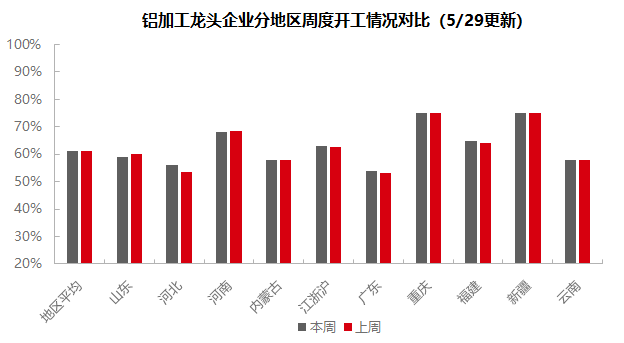

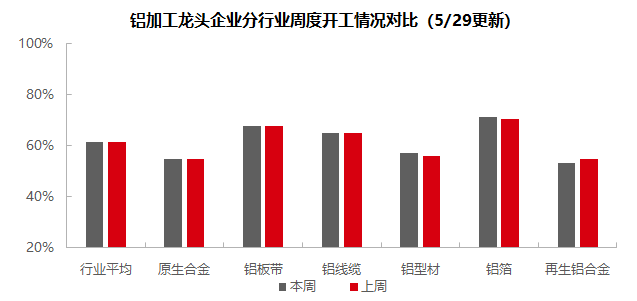

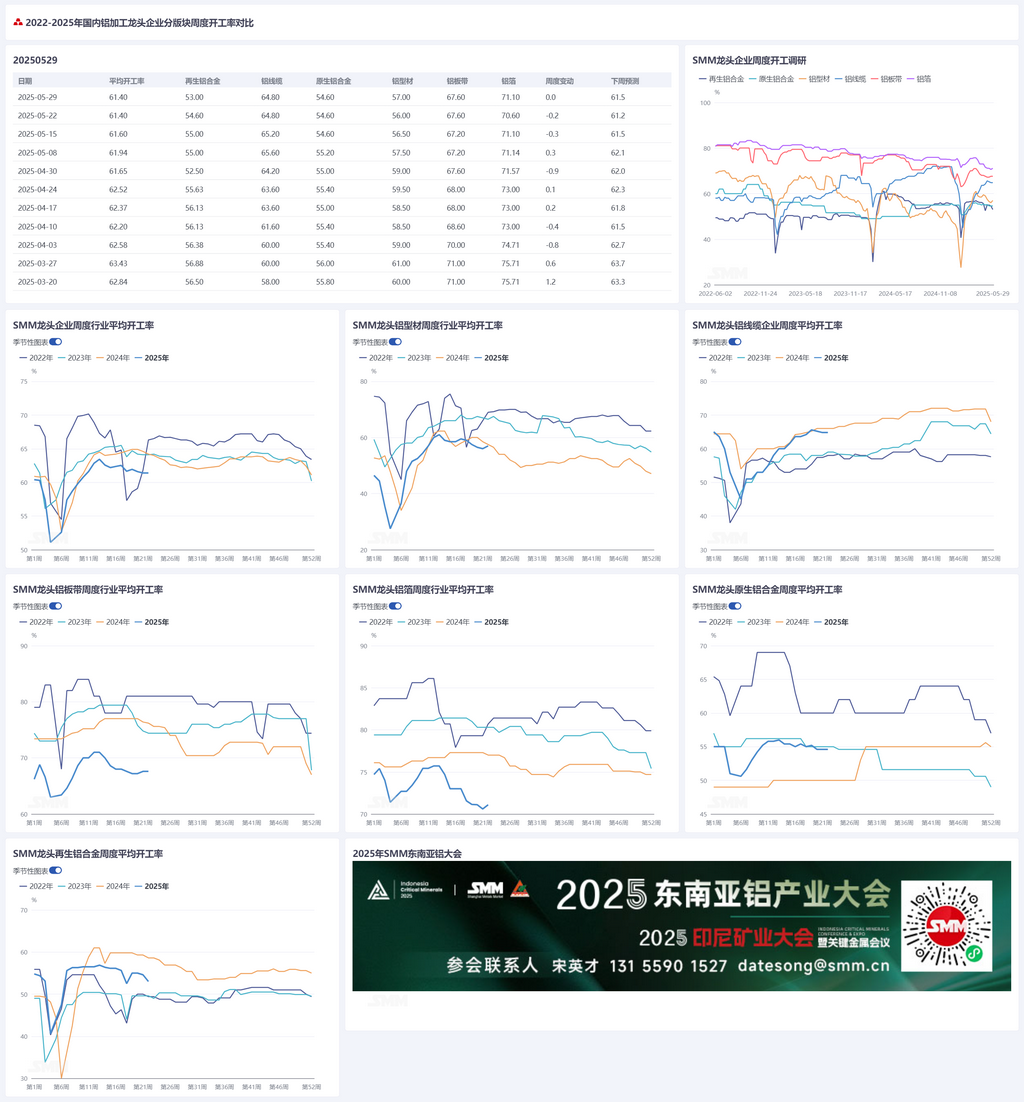

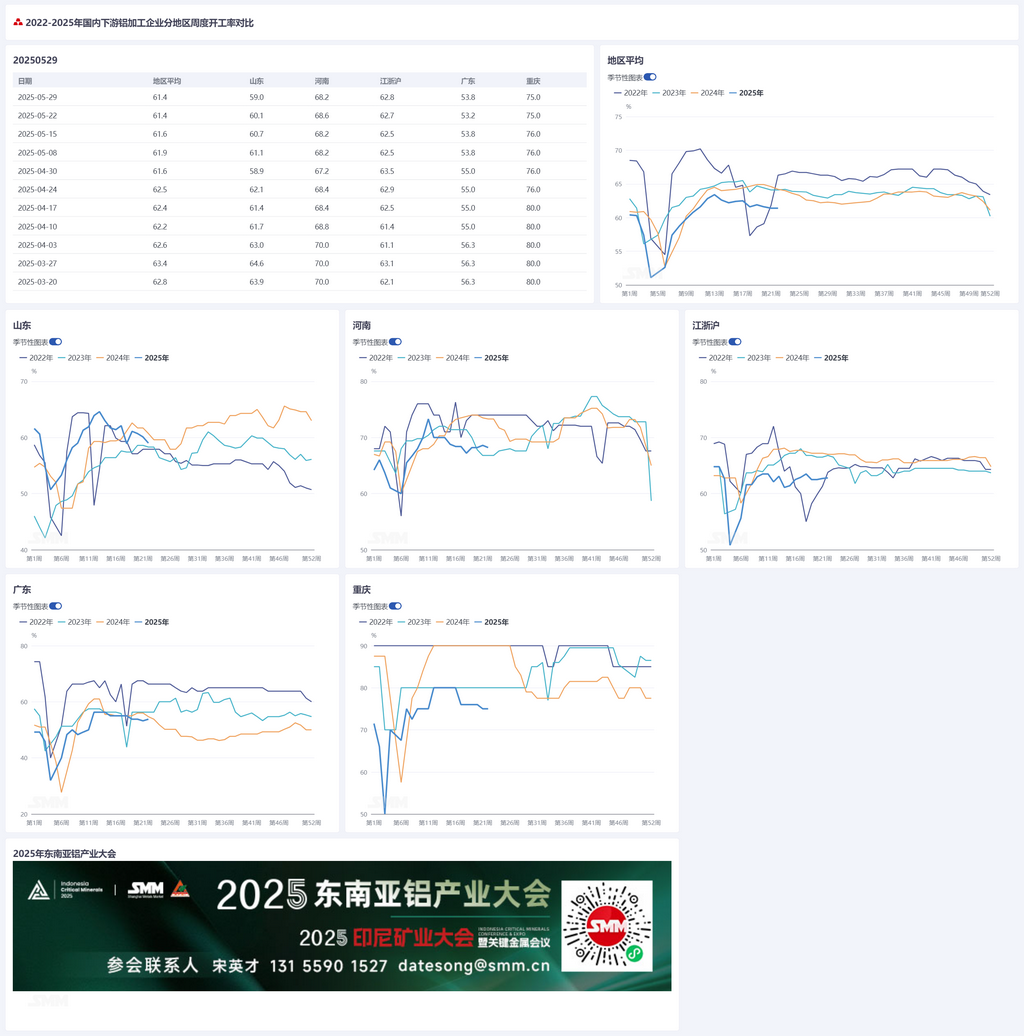

This week, the operating rate of leading downstream aluminum processing enterprises in China remained flat WoW at 61.4%, with continued divergence across sectors. The operating rate of primary aluminum alloy held steady, while export structure saw significant changes (a sharp drop in exports to the US and a surge to Mexico). The rate is expected to remain generally stable with slight fall in June. The operating rate of aluminum plate/sheet and strip recorded 67.6%, supported by end-user orders, with pre-export rush and 618 sales promotions providing additional support. It is projected to remain stable. The operating rate of aluminum wire and cable stood at 64.8%, showing stability, with leading enterprises maintaining steady production schedules while small and medium-sized enterprises were weaker. High-voltage power transmission orders provided long-term support but limited short-term stimulus, and the rate is expected to fluctuate within a range. The operating rate of aluminum extrusion edged up to 57%, with construction materials benefiting slightly from infrastructure projects in northern regions. PV enterprises showed divergent performance (leading firms remained stable while some small and medium-sized enterprises had orders only until mid-June). Automotive extrusion remained steady. The operating rate of aluminum foil stayed flat at 71.6%, with stable orders, and the 618 promotion and summer consumption are expected to drive a slight rebound. The operating rate of secondary aluminum alloy dropped 1.6 percentage points to 53.0%, pressured by insufficient orders and weak pre-holiday inventory buildup for the Dragon Boat Festival. It is expected to continue its weak downward trend. SMM forecasts the operating rate may rise slightly by 0.1 percentage points to 61.5% next week.

Primary alloy: The operating rate of leading primary aluminum alloy enterprises remained stable WoW. Aluminum wheel hub exports in April showed overall resilience, supporting the production resilience of primary aluminum alloy enterprises to some extent. Notably, the export structure underwent significant changes, with exports to the US plunging 18.3% WoW to 5,200 mt, accounting for less than 30% for the first time. This was mainly due to top-tier enterprises' early deployment of overseas capacity in Mexico, Thailand, and Morocco, which not only met new overseas orders but also reduced direct reliance on US exports. As a result, no significant pre-export rush was observed domestically in the short term under traditional trade friction. Meanwhile, exports to Mexico exceeded 10,000 mt for the first time (up 22.7% WoY and surging 44% YoY), highlighting transshipment trade characteristics. Looking ahead to June, considering top-tier enterprises are still assessing orders under the new tariff environment and the upcoming traditional off-season factor, SMM expects the industry's operating rate to maintain a generally stable with slight fall pattern. A substantive turning point will only emerge after details of the latest US-China tariff negotiations become clear.

Aluminum plate/sheet and strip: The operating rate of leading aluminum plate/sheet and strip enterprises recorded 67.6% this week. Leading enterprises remained stable during the week, with aluminum plate/sheet and strip materials linked to end-users such as automotive, home appliance, and kitchenware sectors maintaining normal production thanks to relatively sufficient orders on hand. Currently, during the US-China trade détente, the pre-export rush of aluminum plate/sheet and strip is proceeding in an orderly manner, providing some support to the operating rate. On the other hand, the 618 mid-year consumption period is approaching, with end-users in automotive, electronics, and home appliance sectors intensifying new rounds of price cuts to attract consumption and reduce inventory. However, the actual consumption situation in June still requires close observation, and excessive optimism is unwarranted. The operating rate of aluminum plate/sheet and strip is expected to remain stable in the future.

Aluminum wire and cable: This week, the operating rate of leading enterprises in the aluminum wire and cable sector stood at 64.8%, showing stable performance. As we entered late May, the production schedules of leading enterprises, supported by orders on hand, proceeded steadily, with a robust operating rate. However, small and medium-sized enterprises faced weaker operating rates due to the conclusion of intensive delivery periods and the persistent high prices of raw materials. Despite the delivery cycle of power transmission and transformation orders commencing in May, the staggered deadlines for these orders, which extend into the second half of the year, will provide long-term order support, though the short-term stimulus on operating rates remains relatively limited. In terms of orders, the second batch of winning enterprises for State Grid's UHV projects was officially announced on Tuesday this week, with orders exceeding 2.8 billion yuan and 140,000 mt for ground and conductor wires officially confirmed. Meanwhile, State Grid also issued scattered tenders. In addition to the ongoing delivery of power transmission and transformation orders, the support from overhead line orders in some provinces is slightly insufficient, and there are concerns about the expected growth in new PV orders. It is anticipated that the operating rate will remain within a certain range in the future.

Aluminum extrusion: This week, the national operating rate for extrusions increased slightly by 1 percentage point WoW to 57%. In the construction materials segment, the overall operating rate rose slightly compared to last week. According to the SMM survey, leading enterprises in Shandong and central China reported an upward trend in overall operating rates, benefiting from orders for infrastructure projects in north China (such as Qingdao, Yantai, and Tianjin). Enterprises reported that local government support is gradually being transmitted to the industry. However, some small and medium-sized enterprises in north China and south China reported that infrastructure orders are relatively limited, with their orders on hand mainly related to real estate, resulting in sluggish operating rates. This week, the operating rates of PV frame sample enterprises continued to diverge. Some leading enterprises in east China maintained the same operating rate as last week, primarily due to their cooperation with top-tier enterprises, which allowed their production to remain unrestricted by the 531 period. New orders for June have already been secured, supporting this week's operating rates. Meanwhile, according to the SMM survey, some small and medium-sized enterprises in Anhui reported that, as month-end approaches, their orders on hand for PV frames can only sustain production until mid-June, with no follow-up orders in sight. Their operating rates for PV frames remain at a low level of 30-40%. This week, automotive extrusion sample enterprises operated relatively smoothly with orders on hand. Despite some enterprises in east China and south China reporting that some OEMs have indicated an upward trend in demand forecasts for June, these enterprises believe there will be deviations between actual demand and projected values and will not increase production for the time being. SMM will continue to monitor the actual progress of order fulfillment in various sectors.

Aluminum foil: This week, the operating rate of leading enterprises in the aluminum foil sector reached 71.6%. Orders for aluminum foil products such as battery foil and brazing foil from various producers remained relatively stable during the week. Although relevant data indicates that the overall social inventory of automobiles is currently at a high level, and end-user automakers are facing destocking challenges, the upstream aluminum foil materials sector, including battery foil and brazing foil, may face operating pressure in the future. However, with the upcoming 618 mid-year shopping festival and the approaching summer, consumer terminals such as air conditioners and beverages are expected to see a new round of consumption support, thereby boosting the operating rate of the aluminum foil industry. It is expected that the operating rate of the aluminum foil industry will likely see a slight rebound in the short term.

Secondary aluminum alloy: This week, the operating rate of leading secondary aluminum producers fell by 1.6 percentage points WoW to 53.0%. Insufficient current orders have led to high shipping pressure in the secondary aluminum market, with ADC12 prices continuing to be more likely to fall than rise. As the Dragon Boat Festival holiday approaches, downstream restocking sentiment remains low, with only minimal restocking operations being maintained, providing limited boost to demand. During the holiday, most sampled secondary aluminum plants maintained normal production rhythms, while a few suspended operations for 1-2 days, resulting in a slight downward trend in the overall operating rate. In the short term, secondary aluminum alloy production still lacks upward drivers, and the subsequent operating rate may continue to exhibit a weak downward trend.

》Click to view the SMM Aluminum Industry Chain Database

(SMM Aluminum Team)